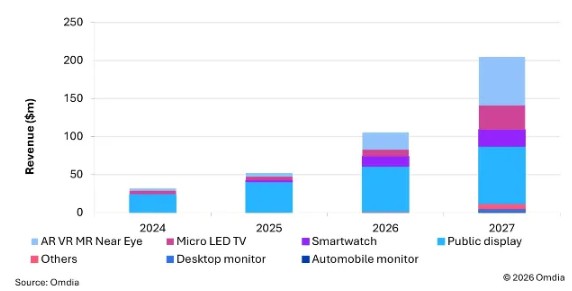

MicroLED display revenue is set for a pivotal year. According to the latest projections from Omdia, global MicroLED display revenue will more than double from $52.4 million in 2025 to $105.4 million in 2026, signaling a decisive shift from experimental deployment to early-stage commercialization.

Although MicroLED products remain limited in volume across public displays, ultra-large TVs, smart watches, and smart glasses, rapid progress in manufacturing maturity and targeted product adoption is now translating into measurable financial growth.

For years, MicroLED development was constrained by several structural bottlenecks:

Recent advancements have reduced these technical barriers. Manufacturers have improved chip uniformity, enhanced transfer precision, and increased overall production yield. As a result, MicroLED TVs, large-format public displays, and wearable devices are entering scaled pilot production.

The most important inflection point is not volume parity with LCD or OLED, but the achievement of repeatable manufacturing processes capable of supporting commercial launches. That transition underpins the projected revenue doubling in 2026.

A major catalyst behind revenue expansion is the rapid development of LEDoS (MicroLED on Silicon) architectures.

Unlike conventional display panels, LEDoS integrates microLED chips directly onto semiconductor substrates. This approach aligns more closely with semiconductor fabrication processes than traditional LCD or OLED manufacturing lines.

Typical LEDoS displays feature:

These characteristics make LEDoS particularly suited to:

Compared with Liquid Crystal on Silicon (LCoS) and OLED on Silicon (OLEDoS), LEDoS offers significantly higher brightness and resolution — two parameters critical for outdoor-capable smart glasses and AI-powered wearable devices.

As global brands accelerate AI-enabled wearable ecosystems, LEDoS is emerging as a preferred display platform.

MicroLED is not positioned to compete immediately in mainstream smartphone or TV segments dominated by cost-optimized LCD and OLED supply chains. Instead, early adoption is concentrated in performance-critical niche markets where competing technologies cannot meet specific requirements.

Key growth segments include:

MicroLED modularity enables seamless large-scale video walls with superior brightness, longevity, and color stability.

Near-eye applications require extreme pixel density with high precision alignment — a strong fit for LEDoS technology.

Next-generation vehicles demand exceptionally high brightness for outdoor readability and HUD integration, exceeding traditional LCD/OLED limits.

MicroLED’s high aperture ratio and luminous intensity enable viable transparent commercial installations.

MicroLED chip modularity supports flexible and surface-adaptive display structures.

These specialized segments create premium pricing environments, supporting revenue growth even before mass consumer adoption.

Despite accelerating growth, MicroLED commercialization remains technically complex.

Mass transfer — involving tens of thousands to millions of microLED chips depending on resolution — fundamentally differs from LCD liquid crystal injection or OLED patterning processes. Additionally, manufacturers must manage:

This complexity requires substantial capital investment, engineering capability, and ecosystem collaboration.

While 2026 revenue will reach approximately $105.4 million, long-term projections are far more significant. Omdia forecasts that MicroLED display revenue will expand to $6.8 billion by 2032, representing around 4.4% of the total flat-panel display market.

This growth curve suggests three distinct phases:

The next 24 months will determine whether MicroLED secures its position as a complementary premium technology — or evolves into a mainstream display platform.

The doubling of MicroLED display revenue in 2026 is not merely a statistical milestone; it reflects structural progress in manufacturing, ecosystem readiness, and application-driven adoption.

Rather than competing head-on with mature LCD and OLED infrastructures, MicroLED is carving out performance-differentiated markets where brightness, resolution density, transparency, and durability are non-negotiable.

If current production gains continue and LEDoS development accelerates alongside AI wearable adoption, MicroLED could transition from niche innovation to a foundational display architecture within the next decade.

For stakeholders across the display supply chain, 2026 will be remembered as the year MicroLED moved decisively from promise to measurable commercial impact.